Correspond with mortgage brokers and you can banking companies that have experience in HELOCs and household build financing

- Such financing is known as one minute-financial, and therefore if you can’t spend, the lender can also be foreclose and work on the main lien proprietor. Or even the lender can sell the home. Also, the construction loan bank is hold back until the fresh case of bankruptcy has finished and sell your house.

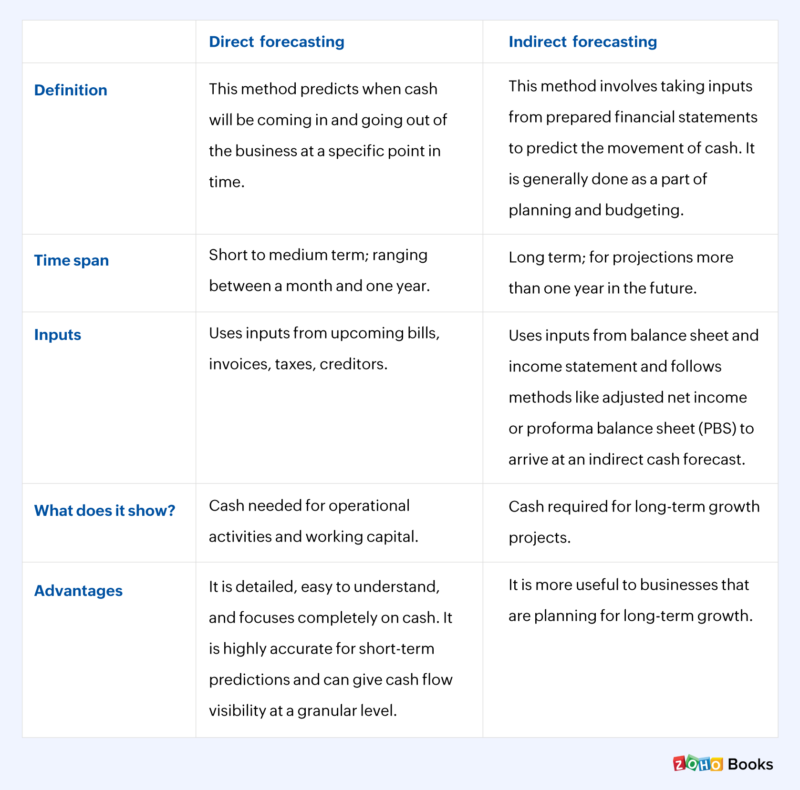

The big versions is the home equity mortgage and the house security line of credit, also called good HELOC). This new guarantee loan choice will provide you with that lump sum off guarantee to cover your home improvements, since the HELOC gives you a line of credit one you could potentially tap since you need it for your home advancements. Whether you are leaning on a conventional framework financing, HELOC or domestic collateral mortgage to create new house, you should know and therefore applications you truly qualify for that have your current borrowring back ground. It is vital to when considering the development loan versus range out of borrowing that you know the new closing costs, rates and you will loan amount limitations before choosing an alternative.

Hence Loan Style of is better getting Family Design (Do-it-yourself Financing compared to. HELOC)

It all depends abreast of your position. Getting a homes or do it yourself mortgage enables you to would renovations but it’s with the an appartment agenda in addition to cash is disbursed of the bank while the specific goals was met.

Also, the construction mortgage is of a restricted duration, which have financing chronilogical age of less than six years are extremely well-known. This can increase the amount of their monthly installments.

However, into the right up front side, your rate of interest can be repaired and you can produce spending quicker attract throughout the years given the brief lifetime of the brand new mortgage.

To have performing home improvements, there’s little doubt you to definitely a property collateral financing or family guarantee line of credit is among the most preferred. Financing reliant your own house’s collateral will give you a low interest rate, nonetheless it is a bit greater than your first home loan rate of interest.

If you opt to get a great HELOC build range, you’ll pay appeal simply repayments into the first four otherwise 10 years of the loan, and therefore the rate of interest have a tendency to dive since you beginning to make idea costs as well. Property guarantee financing provides a predetermined price.

availableloan.net/loans/private-student-loans

If you get good HELOC, a security mortgage otherwise a money back refinance, you are going to spend the money for financing more than age, that’ll reduce your monthly installments. not, make an effort to shell out far more within the notice than a beneficial build otherwise home improvement loan. See the latest HELOC rates and you will household guarantee financing borrowing from the bank out-of federal financial institutions.

Congress introduced a taxation reform costs that eliminates the ability getting residents to track down an income tax deduction to own a home security loan during the 2024, making it important that you take into account the positives and negatives off a casing mortgage in the place of a house collateral loan prior to signing data.

How to Qualify for a housing Mortgage

If you get a home loan to create your home, the lending company doesn’t always have property as the collateral throughout the construction. This is why being qualified to own a housing financing or credit line can be more hard. The building financial should find details about the size of your house, the information presented that were made use of additionally the designers that will be doing the job. Your overall builder can offer the information wanted to fulfill the lender.

The lender needs in order to remember that it is possible to purchase the newest month-to-month mortgage costs as your home is situated. In case the financial thinks that you are not able to shell out your home loan or book since house is are established, you might not obtain the structure mortgage.